Perspective

Reimagine the banking customer journey

Sajit Vijayakumar

Chief Operating Officer, Infosys FinacleIntroduction

A bank in New Zealand allows customers to park their savings in customized buckets named after goals, such as a “Machu Pichu”, “Prada Bag” or “Rainy Day”. In the United States, USAA provides not just housing loans, but also third-party assistance to help military families find homes and related services catering to their unique needs.

These are examples of banks that are beginning to view their relationship with customers from the latter’s point of view. Customers rarely view banking as an end in itself; to them it is a means that serves a larger purpose, a process embedded within daily activities or life events. The bank is simply a transit point for customers on different journeys.

Mapping the customer journey is therefore an essential (and rewarding) part of experience transformation. Recent research shows that 85 percent of those who practice it have experienced a positive or very positive impact. Benefits include higher customer satisfaction, fewer customer complaints and lower churn. New-age organizations, and especially big-tech firms like Google, Amazon and Apple, are living examples of businesses that owe much of their success to their beautiful customer journeys. Banks seeking to reimagine their journeys and customer experiences to big-tech standards should look at doing the following:

Given that banks are awash in information today, it is very important to identify the data sets of relevance.

Do more with data: Most banks already use their data to personalize the customer journey by customer segment. (For instance, a high net worth customer is ushered quickly past the queue to the branch manager). The next step is to personalize the journey (or communication or experience) to the individual customer, much like Netflix or Amazon does through targeted recommendations. Once a bank is past this stage, it can look at exploiting data further for things such as improving its pricing model. Here, the dynamic pricing model of companies such as Uber could provide food for thought.

A word of caution. Given that banks are awash in information today, it is very important to identify the data sets of relevance. For instance, Amazon’s personalization engine considers a customer’s purchase history, reviewed products, and other purchases made by buyers who bought the same item as this customer, ahead of other information. In the case of a retail bank, point of sale data or purchases made by customers who behave the same way, enjoy a similar lifestyle or are at the same life-stage must inform customer journey personalization.

Think tech: A bank might have the right ideas and data for improving the customer journey but the wrong technology could let it down. It must therefore choose its platform judiciously – in terms of technology, scalability, reliability and support – and also employ the right algorithms. Spanish bank BBVA is doing it right with an algorithm that uses a customer’s product portfolio, geographic location and other factors to personalize in-app experiences.

Chinese insurer, Ping An, has gone a step ahead to recast itself as a technology company with a license to conduct a financial service business. It is using technology to insert its presence into customers’ everyday journeys.

A better approach is to think about technology the way the best technology companies do – as something that is embedded within every process, application, innovation, idea or customer journey. It is not enough to merely onboard the best-known customer journey mapping vendor or use the most suitable digital banking solution; the bank must think about its impact and integration with surrounding processes and applications.

Chinese insurer, Ping An, has gone a step ahead to recast itself as a technology company with a license to conduct a financial service business. It is using technology to insert its presence into customers’ everyday journeys. Whether it is a quest for better health, better transport, or even better entertainment, Ping An has a platform business and ecosystem connections (and of course an insurance product!) to facilitate the journey.

Journey by design: Onboarding, transaction, service and resolution are all parts of banking journeys. However, customers view banking as a part of the broader life journeys they take to fulfill various needs. Banks must reciprocate that thinking by participating in these larger journeys by being present right from the time the customer acts on a primary need (need for wellness rather than medical insurance; need for vacation rather than travel card etc.). Banks like DBS are already doing this by setting up a marketplace platform for buying and selling pre-owned cars.

As is clear from above, primary needs and significant life-stage events – marriage, parenthood, home buying – make for the most obvious customer journeys. However, by employing techniques, such as Design Thinking, a bank can become more empathetic to customers and discover new journeys. The presence of ecosystem partnerships is key to this, of course, but so is a well-timed intervention.

For instance, when a bank is already facilitating a customer’s house purchase through partnerships, it can initiate more journeys with recommendations for legal services, packers and movers, utility companies and interior decorators at the precise time they are needed.

Reimagining a customer journey is not a one-time activity. It calls for constant innovation and several iterations. When there are competing ideas, it is wise to test them in parallel (using A/B testing etc.) before choosing one. Amazon is one example of a company that tests its shopping experience processes constantly to eliminate friction.

Open up to opportunities: The move towards open banking is forcing the universal bank – one that manufactures, owns and distributes products and services through its own channels – to adopt a platform business model where it sources, aggregates and distributes a variety of financial and non-financial offerings using a network of partners from an ecosystem that it might even help to build.

Banks must embrace this trend by working with partners to innovate and expand their range of offerings, and by leveraging those tie-ups to expand, fulfill and enhance their customers’ life journeys.

The last word

As the customer journey becomes more crucial in the banking relationship, non-banking players, especially bigtech companies and FinTech challengers, might seem to have an edge. But while these new-age entities may have mastered the customer journey, banking incumbents must draw comfort from their own inherent strengths, including but not limited to, vast financial resources, loyal user base, expertise in regulatory compliance, reputation, and customer trust. By reimagining their customer journeys, banks can mitigate both friction in customer experience and the advantage of their young rivals to reclaim their supremacy in the market.

Download FinacleConnect

FinTech innovation in banking

The case for greater collaboration

Ravishankar

Chief Executive Officer, Active.aiCreating new experiences in banking: A transformation journey

Puneet Chhahira

Head of Marketing & FinTech Engagements, Infosys FinacleExploring the relationship between customer satisfaction and financial performance has consistently been a pursuit of interest for researchers. And their findings have consistently revealed a clear correlation – businesses that report higher customer satisfaction also report stronger financial performance. Recent research by the Institute of Customer Service states that organizations that maintain a customer satisfaction score above their sector average achieve 9.1% revenue growth year-on-year while those with a lower-than-average customer satisfaction score achieve just about 0.4% growth year-on-year. The positive top-line growth is a function of favorable customer retention, customer acquisition and cross-sell/up-sell outcomes. The right customer experience keeps the existing customers returning for more, as they also double up as advocates positively influencing the rate of new customer acquisition. What’s more, great CX directly translates into benefits of lower total cost-to-serve. For one, expanding the existing share of customers’ wallet is a more cost-efficient means of meeting revenue goals than putting all weight behind chasing new customers. A proven fact, industry regardless. Secondly, one of the key enablers of great digital customer experience is the use of technology and automation, which if done right, can help save millions in the cost-to-serve.

Clearly, good customer experience is good business. And technology and business executives recognize this. The ripple effects of CX improvement across customer acquisition, retention, sales and cost-to-serve metrics have been widely acknowledged in business and technology circles. However, many an executive seem to be losing the plot somewhere between “recognizing the importance” and “translating it into the required action”. In financial services, all senior industry professionals admit to a willingness to radically improve customer experience, but few seem to have charted a definite approach or demonstrate the sense of urgency essential to drive the transformation efforts.

When it comes to customer experience transformation, few things are more important than understanding what a great customer experience means to a business, in its unique business context and environment. That is to say, defining the right vision to know where one wants to go is paramount. Next, it is equally crucial to determine the level of competency required to deliver on that vision. The total competency quotient (TCQ) is not limited to financial or technology considerations but cuts across people, processes, operations and technology. An unbiased and honest assessment of the existing level of competency uncovers the gaps and sets out the direction for a roadmap that is realistic and pragmatic, yet aligned to the long-term vision.

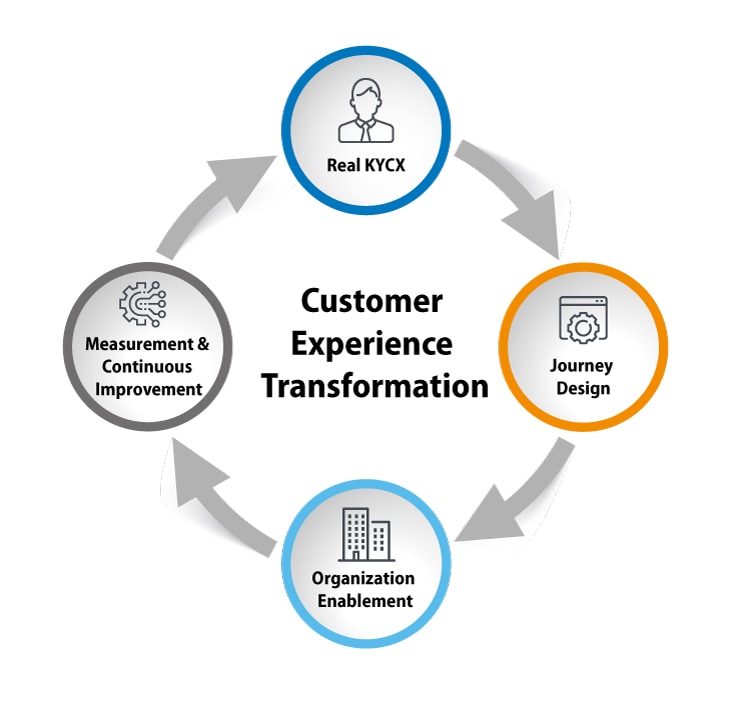

In our view, they are four fundamental rungs to this transformation ladder:

1. Real KYCX (Know your customer’s experience)

A customer experience transformation initiative is highly likely to come a cropper if it begins with an inaccurate understanding of the current customer experience, no matter how clear and bold the vision. This crucial first step in the process is what we call the “Real KYCX” stage. And doing this right requires banks to perform a comprehensive analysis and assessment that takes into consideration insights from quantitative as well as qualitative methods. Techniques that provide a fresh stream of real-time data inputs such as recording journeys for web and mobile analytics can be particularly instrumental in discovering where customers abort a journey, take longer than the average estimated time or diverge from the expected path. Qualitative inputs such as customer interviews often serve to correct any false positives and reveal the deviation between the perceived and the actual level of customer satisfaction. Real KYCX is not about “more data” but about “the right data” gathered through a combination of quantitative and qualitative techniques.

Leading banks are restructuring their CX organization around customer journeys. The practice prevents handshakes across various functions, since each journey team comprises a diverse set of experts across product development, business development, channel strategy, and more.

2. Customer journey design

The Design phase spans several sequential steps such as persona building, workflow and data flow design, and design thinking-led journey map design. While the importance of flawless planning and execution across all these stages cannot be overstated, the journeys a bank prioritizes can go a long way in demonstrating immediate value of change to the customers.

A customer’s experience with a bank is the sum total of all the experiences and interactions the customer has with the bank. However, not all customer journeys are equally critical or important. Prioritizing some over others can hold banks in good stead. In fact, a rewarding practice many banks seem to be adopting now, is aligning and driving multidisciplinary effort towards re-imagination of identified customer journeys. Instead of organizing talent in functional units, leading banks are restructuring their CX organization around customer journeys. The practice prevents handshakes across various functions, since each journey team comprises a diverse set of experts across product development, business development, channel strategy, and more. Prioritizing journeys helps drive dedicated cohesive effort towards re-imagining the identified customer journeys.

An excellent transformation strategy that does not figure a plan to enable all stakeholders in the value chain to adapt to new ways of working is like attempting to steer pods designed for a steam-powered carriage at hyperloop speed.

3. Organization culture and workforce enablement

An excellent transformation strategy that does not figure a plan to enable all stakeholders in the value chain to adapt to new ways of working is like attempting to steer pods designed for a steam-powered carriage at hyperloop speed. A business or organization transformation is not about how progressive, agile, and efficient its innovation engine or innovation team is, but how quickly and effectively employees in the organization can understand what change means for them at an individual level, and then create value in their respective roles, responsibilities, and circles of influence. The business has a large and critical role to play in this transformation. When Singapore’s leading bank DBS embarked on its transformation strategy in 2015, people and culture transformation was not an afterthought but a project run concurrently with technology transformation. The bank’s three-part approach to workforce and culture transformation called “Think Digital” encompassed learning through education, learning through experience, and learning through exposure. The bank educated its employees on digital business models, human-centered design principles and journey thinking using the 4D framework (discover, define, develop, deliver) and agile methodology; implemented the squad model for experience-led learning; and, chose a select group of employees to act as Digi Ninjas to expedite adoption and eliminate barriers. Continuous learning forms the core of workforce upskilling and transformation efforts of Infosys. Wingspan, a next-gen enterprise learning solution, is not only used widely within the organization but has also been adopted by a few leading banks in the U.S. for talent transformation.

4. Periodic measurement

KPIs such as customer satisfaction index (CSI) and net promoter score (NPS) are evidentiary indicators of customer experience success. But what can significantly enhance these final indicators is a regular measurement of performance against the key parameters identified and measured during the “Real KYCX” stage. Employing qualitative and quantitative techniques comprehensively to measure performance across the identified metrics helps track and benchmark improvement. What’s more, a rigorous performance improvement discipline informs decisions in the event an identified pursuit warrants course correction.

Conclusion

The industry is in the midst of multi-dimensional change. With the rise of new collaborative models, the unbundling and re-bundling of products and propositions is dramatically changing the supply-side dynamics. On the demand side, the empowered and digitally-savvy customer is interacting with financial service providers in new ways and on a variety of new digital channels. Re-imagining customer journeys for this change begins with an accurate understanding of the current level of satisfaction of a bank’s customers. As stated, a combination of qualitative and quantitative techniques to arrive at the true picture sets out the direction for transformation. Translating these insights into action requires the right priority matrix and the introduction of related organizational changes to drive swift execution. Next, true customer-centricity requires every employee in the organization to understand how they can drive positive customer outcomes within the context of their roles and responsibilities. A customer-centric organization is one that relentlessly focuses on organization-wide learning and development to keep pace with the rapidly changing customer expectations. And finally, defining the right yardstick and measuring performance regularly provides the benchmark and impetus to drive continuous improvement.

Banks may choose to prioritize different journeys based on their unique realities. However, an accurate understanding of these realities is the first step towards successful CX transformation.

Four key essentials of sustainable CX transformation in banking

Rajashekara V. Maiya

Vice President, Business Consulting and Product Strategy, Infosys FinacleCX and customer onboarding A reality check for banks

James Buckley

Regional Director, Europe, Infosys FinacleA tale of two journeys

Abhishek Verma

Senior Director and Digital Evangelist, Infosys FinacleIntroduction to the customer journey

Open Banking, and its key enabler, the platform business model, are ushering unprecedented possibilities for customer experience and engagement in banking. With banking services integrating further with daily life activities in the open era, the banking customer experience is also expanding from a one-off event to a journey of connected, not isolated episodes.

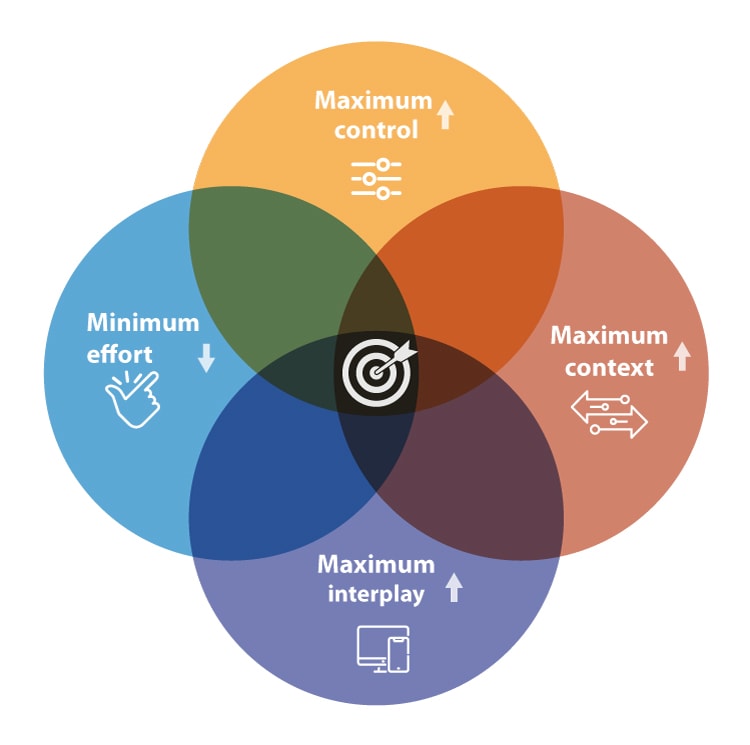

Research by a leading market research and advisory firm says that customer journey analysis is a top priority for the customer analytics initiatives of enterprises. Designing the right journey for an open banking environment is therefore of utmost importance. An effective customer journey has the following attributes:

Two journey scenarios

The customer journey in an open banking era is superior to the banking experience of the past in every way; it is more convenient, more engaging and has infinite possibilities. The following two scenarios clearly illustrate the difference.

In the first scenario, Christian, a financial controller at a medical devices company, travels from California to New York for a business conference that he has registered for on BusyConf, which is integrated with his savings bank account at Lloyds Bank, and paid for via Zelle, Bank of America’s P2P payments app. At New York airport, he calls for an Uber car to reach his hotel; on the way, he checks on booking.com whether the hotel has agreed to allow him early check-in.

The next day, an important Dutch client asks for a meeting on the coming Friday, a day after the conference in New York ends. Christian scrambles to reschedule his British Airways flight through the bank’s mobile app, and is lucky to find a seat in the busy weekend traffic.

On Friday evening after the meeting, he shops for some specialty cheese and stocks up on Stroopwafel at Albert Heijn. Realizing that he does not have enough diabetic medication, he orders some through the bank’s iphone app, thanks to its integration with a pharmacy app.

Just for fun, he checks a BBVA app called Bconomy to see if he bought these items at a good price; it’s the same app he will use later to reconcile his travel expenses, some of which he paid from his own pocket.

The second scenario features Kathy, a communications manager, who is looking to buy her first house. She asks the smart assistant on the Rightmove app on her iPhone to find a suitable flat costing about GBP 500,000 close to Canary Wharf. Her spoken command launches a search that throws up several housing options; when she likes something, the app proactively triggers a search for a mortgage at a comparison site, based on her financial status and loan eligibility. All this is possible because the mobile app of Kathy’s primary bank is integrated with the apps of a number of service providers in the home buying value chain. (Should Kathy accept one of the mortgage options, a loan application will be triggered automatically and the chosen mortgage provider, which is linked via APIs to Kathy’s bank and also to various credit rating agencies, will give a decision within 48 hours.) Then her banking app triggers the next stage of her journey, where legal advisers, real estate solicitors, relevant government bodies, etc. come in to facilitate the purchase. Other triggers are sent out to providers such as movers and packers, home stores like IKEA, and also to utility companies informing them of the impending move. Kathy starts to receive offers on her mobile phone, and when the time comes, she can simply choose the best ones. Job done.

While this seems like a customer journey from the future, a number of digital innovators are already working on it. If a bank were to integrate APIs from companies such as niki.ai, it would be able to cater to every need in the home buying customer journey through its own (single) app. That’s one app for everything, from buying insurance and comparing rates to dealing with legal service providers, packers and movers, furnishing retailers and utility companies.

Compare this amazing customer journey in an open banking environment to the traditional home buying experience where Kathy would have had to find and deal with each of these agencies separately. Open banking not only simplifies and accelerates the entire process, but also amplifies the value derived by the customers and the members of the provider ecosystem.

Closing comment

As is clear from the scenarios, both Christian and Kathy manage to access a variety of apps and perform the diverse transactions in their journeys using a single mobile banking app from their primary bank. This is already becoming possible in the open banking world where the different mobile apps of different providers offering different services can be integrated via APIs with a single banking app. And thanks to the geo-location capabilities of the underlying software, any customer journey can run smoothly in parallel with the customers’ physical journeys, even when they are crossing countries and continents.

Corporate banking Seeking new journeys, new destinations

Sudhindra Murthy

Global Product Marketing Manager, Infosys Finacle