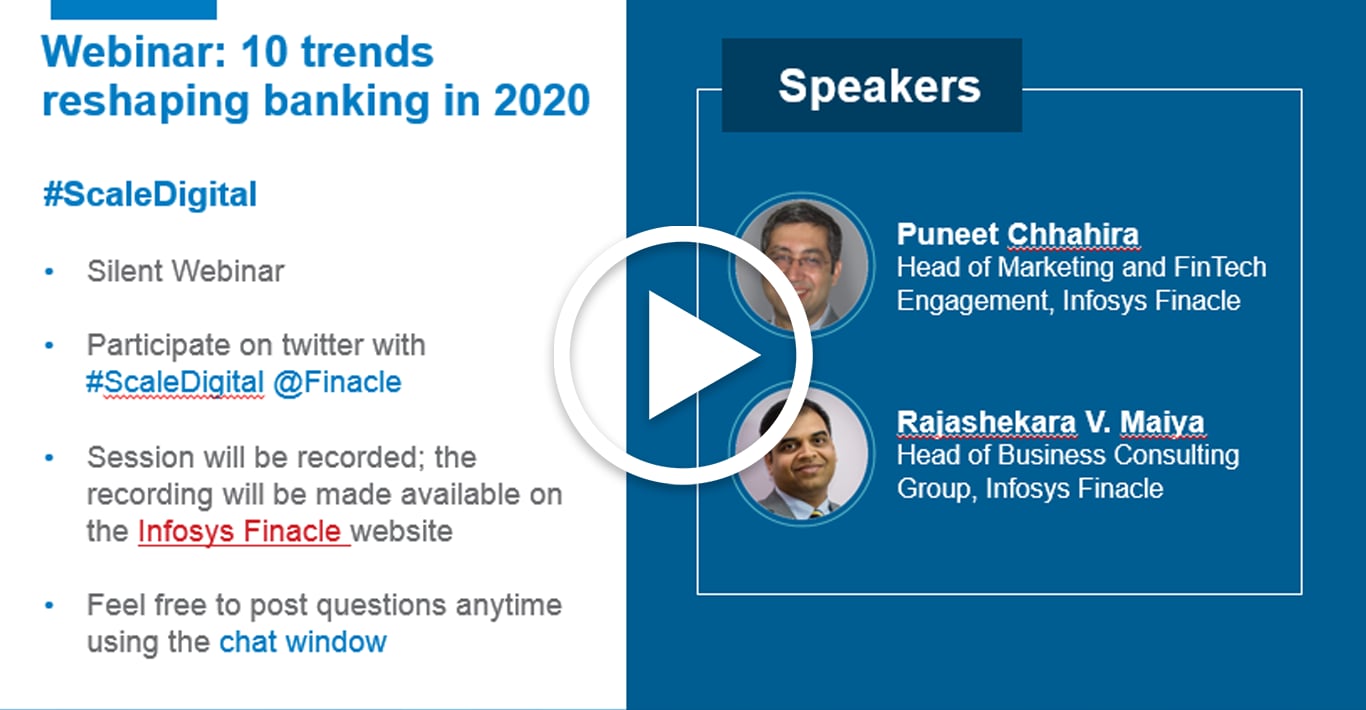

Webinar

Scale Digital: 10 Trends Reshaping Banking in 2020

What does it take for a bank to #ScaleDigital across all the five critical areas: business model, organization, automation, technology, and culture? What will be the key shifts in 2020? What are transformation leaders doing right and what will they change in 2020?

Watch the webinar recording to learn the key trends banks like yours will need to scale transformation journeys in 2020.

Trend #1 | 2020: The year the business model changed

In an exceedingly commoditized market, banks are beginning to make clear bets to become leaders in scale, value, customer experience or product / service excellence. Some are turning into specialist providers: manufacturers of market-leading products, aggregators, distributors, segment players, or banking-as-a-service providers. However, in the 2019 Innovation in Retail Banking study by Efma and Infosys, as many as 50 percent of respondents stated their intention to continue as full stack banks. Will that change in 2020?

Trend #2 | Citius, altius, fortius with Agile in 2020

A truly agile organization in 2020 and beyond will be a sum of various self-learning, self-healing, and self-evolving parts, each of which works in tandem with the other through suitable gateways for collaboration. Much like a living organism that evolves, adapts and self-learns, more and more organizations will live and breathe Agile in 2020. The Agile way of working in 2020 will pervade technology, operations, talent practices, business strategies, leadership, and ecosystems.

Trend #3 | Automation in 2020: Alive and well and everywhere

The outlook for automation in 2020 and beyond remains strong, amid continuing pressure on margins. And RPA is one technology that most banks have deployed successfully. Some progressive banks are now using RPA in the shape of co-bots to improve workforce management, regulatory compliance and customer satisfaction. These robots are so integrated within the workforce that they have IDs like other employees, and are able to seamlessly take over or hand over tasks midway to their human co-workers. What’s next? Banks coming together to pool resources and automate non-differentiating functions? Read our forecast.

Trend #4 | 2020: The bank of the millennial workforce

As AI and automation become more deeply entrenched in the banking organization, it will be the responsibility of the human workforce to compound value through critical thinking, collaboration, creativity, and effective communication. In 2020, banks will train the workforce to hone these skills. The most successful organizations will create – or sustain – a culture that unites their people in a shared purpose.

Trend #5 | 2020: The year of security dichotomy

Our 2019 security forecast identified data privacy regulation and Artificial Intelligence-led attacks as the key themes. In 2020, the trends in cybersecurity will derive substantially from those in cloud computing, digital identity, 5G and the Internet of Things, and automation/ AI/ Machine Learning. Regulation will remain an important, and possibly, the trickiest trend to negotiate in the New Year. Some trends will work in opposition to others, forcing banks into a delicate balancing act. How will these trends play out? Read our forecast for cybersecurity trends in banking.

Trend #6 | Technology in 2020: Information, application, and the whole nine yards

Leaders, fast followers, and mainstream players all recognize that data, advanced analytics, and artificial intelligence will be at the center of consumer engagement and consequently market success over the next few years. How can banks ensure readiness of their IT architecture, application architecture, system architecture, and information architecture to suit the requirements of the customer-first digital age?

Trend #7 | AI in Banking in 2020: Settling In

AI has been and will continue to be an efficiency lever in banking. In customer service, banks will improve personalization and service recommendations at scale with AI in 2020. The technology will also find application in regulatory functions, given the stringent norms surrounding KYC and customer authentication. Read our trends forecast for AI to know the other significant developments to watch out for in 2020.

Trend #8 | Public Cloud in 2020: New frontiers of flexibility

Declining apprehension against the public cloud, a rapidly growing market for SaaS solutions, and the widespread adoption of cloud as the preferred environment for workload execution. Clear signs that cloud in banking is here to stay? That’s probably a no-brainer now. What are the key trends in the adoption of cloud as the crucial catalyst of co-innovation and integration in 2020? Containerization? Greater flexibility as banks begin to see multi-cloud environment as a solution to performance, compliance, and cost-optimization challenges? Read our trends forecast to know more.

Trend #9 | Blockchain Gets Real in 2020

After successful demonstration of proof-of-concept and proof-of-value, Blockchain began delivering clear and indisputable benefits in 2019. In 2020, while proven use cases in trade finance, payments and identity will continue to see investments, the push for adoption coming from new use cases which justify the large-scale transformation and replacement of systems of record will also pick up pace. Moving beyond the promise of cost reduction and unparalleled efficiency, banks will discover the technology’s potential to reduce risk, build stickiness within their ecosystems, and even generate revenue. How? Read our forecast to find out.

Trend #10 | IoT in 2020: Banking on Every Device

In 2020, banks will explore and tap into the benefits of IoT to offer context-aware guidance and advisory services at the point of transaction. Use cases in fraud detection will include real-time alerts in case the location of a credit card transaction does not correspond to that of a customer’s smart watch or phone. What are the other ways adoption of IoT will unfold in 2020? And how will banks navigate the challenges of data governance, integrity and security as custodians of customer data?

View Infographic Read Full Report

IoT in 2020: Opportunities and challenges abound thanks to explosive growth of connected devices

Read Full Report

Please provide below details to download the report.

Thank you for downloading!

If the download hasn’t started automatically, please click here to download